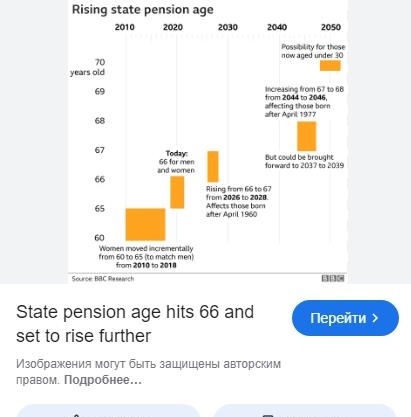

The UK Government’s decision to raise the State Pension age to 67 between 2026 and 2028, and then to 68 between 2044 and 2046, is a very smart way to make sure that the retirement system is fair and will last as life expectancy rises and the economy changes. This slow change is a cautious balance between demographic reality and fiscal sustainability. It is meant to help generations now and in the future.

Because people are living longer and healthier lives, they are naturally retiring later. The 2005 Pensions Commission suggested raising the retirement age to keep things fair, since each generation spends about the same amount of time working and retired. Since then, laws have steadily put these increases into effect, making changes that are perfectly in line with new data on life expectancy and workforce patterns.

This isn’t just a small shift in the way things are done; it’s a strategic alignment, very much like how a swarm of bees adapts to changes in the environment to stay alive. The government’s continuous and competently led evaluations, including the recent third State Pension age assessment, show that it is committed to making decisions based on facts. Age limits are carefully set to match changes in life expectancy and the health of the workforce.

The progressive increase in the State Pension age is important since it means that people born between 1960 and 1961 would have to wait longer each month instead of suddenly jumping to a new age. This careful approach gives people time to arrange their finances and make changes. In the meanwhile, measures like the triple lock guarantee keep pension values safe by tying increases to wage growth or inflation, which keeps pensioners’ earnings fairly stable.

Extending the working life is a smart strategy to deal with demographic difficulties since it eases the strain on the National Insurance system and public pension funds while encouraging people to keep working, which keeps productivity and tax revenues up. Countries all across the world are using similar strategies to deal with their aging populations, which shows that this approach works well in many situations.

This change is a call to action for people: verify your individualized pension estimates, change your savings goals, and think about phased retirements or longer careers. Employers and governments also have important jobs to do. They should create workplaces where older workers may thrive both physically and intellectually. They should also change retirement from a definite end point to an opportunity for continued contribution and a better life.

**Important things to know about the hike in the State Pension age:**

1. **Schedule:** The State Pension age goes up to 67 between 2026 and 2028 and to 68 between 2044 and 2046. It will be checked often to keep up with changes in life expectancy.

2. **Historical context:** The age at which women can retire, which used to be 60, is now the same as the age at which men can retire, which is 65. This is because life expectancy is going up.

3. **Economic reasoning:** Raising the retirement age reduces the strain on public pension spending and stabilizes financing as the population fluctuates, making sure it lasts.

4. **Impact on individuals:** Eligibility depends on exact birthdates, so people need to use government resources to keep track of and plan ahead to avoid surprises.

5. **Protecting value:** The triple lock guarantee makes sure that pensions go up with wages or inflation, which helps keep living standards high even after retirement.

6. **Ongoing review:** The government promises to use data and experts to do regular reviews, keeping a balance between what people need and the health of the economy.

When viewed this way, the rising State Pension age is not a problem but a forward-looking, very effective way to balance equity, economic stability, and personal safety. It encourages us to view retirement as a period of prolonged opportunity and enduring contribution rather than a definitive termination.